Australia’s traditional peak property listing window is upon us. Every year during the first half of March – referred to as weeks nine to 11 on the calendar - there is a surge in listing activity. But not in 2023.

Listings provide a useful real time indicator of seller sentiment and general market confidence. However, this year sellers have erred on the side of caution before listing and the trend is moving lower again with the flow of new listings consistently below average since spring last year.

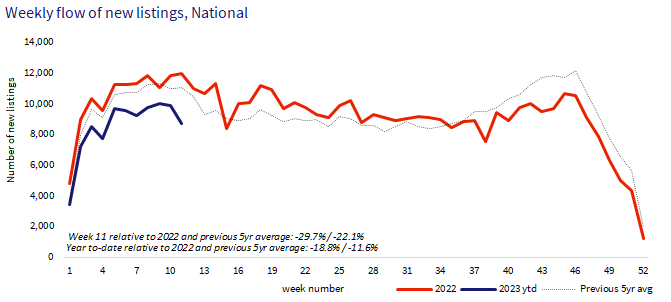

This year 8,721 new listings were added to the market in ‘week 11’ (March 11-19), down 27.3% compared to the same time last year, and 21.3% below the previous five-year average. So far in 2023 new listings nationally have been tracking 18.0% below 2022 levels.

Listings vs housing values

The lower than average flow of fresh stock added to the market is likely to be a key factor supporting housing values. For the past month, CoreLogic’s Daily Home Value Index (HVI) has shown in some cities a lack of new stock has stemmed the decline in values. Sydney housing values in particular are up 0.9% over the past 28 days just as the volume of new listings falls almost 40% year-on-year. It’s a similar story for Melbourne, Perth and Brisbane where housing values are edging slightly higher, or have steadied.

Second wave of listings unlikely

There’s a good chance the flow of new listings has moved through a seasonal peak. Historically, weeks nine to eleven mark the seasonal high point in the flow of new listings before the trend eases leading into Easter and the cooler months. Activity across CoreLogic’s RP Data platform, where real estate agents generate reports to prepare properties for sale, has consistently tracked below levels of the past two years and is once again trending down, indicating fewer properties are being prepared for sale. The year-to-date has seen 14.9% fewer real estate agent reports generated relative to the same time last year.

New listings lowest in the largest capitals

The new listings trend varies from region to region, but most areas of Australia are recording a lower than normal number of fresh listings, especially the largest capitals. The lowest amount of new stock over the year-to-date, relative to the previous five-year average, can be seen across the three largest cities.

- Sydney new listings are 13.2% below the previous five-year average and almost 23% lower than a year ago.

- Melbourne new listings are 12.3% below the previous five-year average and 23.4% lower than last year.

- Brisbane new listings are 17.8% lower than the previous five-year average and almost 20% lower than a year ago.

It seems prospective vendors in these cities are doing their best to wait out the downturn, preferring to hold off on their selling decisions until conditions improve and some certainty returns to their decision making.

Capital city exceptions

Bucking the trend of lower listings through the first 11 weeks of the year is Hobart, Darwin and the ACT. In Hobart, where advertised stock levels are rising from a low benchmark, new listings are up 6.2% on the previous five-year average and 8.9% higher than the same period a year ago. New listings are 7.5% higher than average in Darwin (but almost 20% lower than a year ago and well below the highs recorded in 2014 and 2015) and 2.0% higher across the ACT (but almost 11% lower than a year ago).

Vendor stand off

Watching the ebb and flow of new listings will be a key factor in the performance of this year’s housing market. Arguably there has been an accrual of pent-up supply since September 2022 as prospective vendors delay their selling decisions, possibly frustrating buyers with a shortage of options. However, any sign of a rebound in new stock on the market could trigger renewed downwards pressure on housing values, unless the increase was absorbed by a commensurate uplift in buying activity.

Meet Tim Lawless

Executive, Research Director, Asia-Pacific

Tim is executive research director of CoreLogic’s Asia–Pacific research division, managing a team of economic and data specialists across Australia and New Zealand. He brings more than 20 years’ experience to the role, providing deep insights and analysis on national housing trends.

Full profile