In today’s Pulse, Head of Research Eliza Owen explores the dynamics of property investor activity.

- New investor loans are up a strong 18.8% nationally, far outpacing the volume of investment properties coming to market.

- There are regional differences with the number of investor listings coming to market elevated in Tasmania, Victoria and NSW, but are below average in SA, QLD and WA.

- The number of new loans for investment property purchases is strongest in high capital growth states, showing a pivot in investment to SA, QLD and WA.

- Investor types may be changing with less leveraged investors and more first home buyers entering the market to get on the property ladder.

There are two main narratives about Australian housing investment in 2024 that seem to contradict each other.

One is that investors are giving up on the property market. Existing investors have been turned off by high interest rates, tenancy reform and increased property taxes.

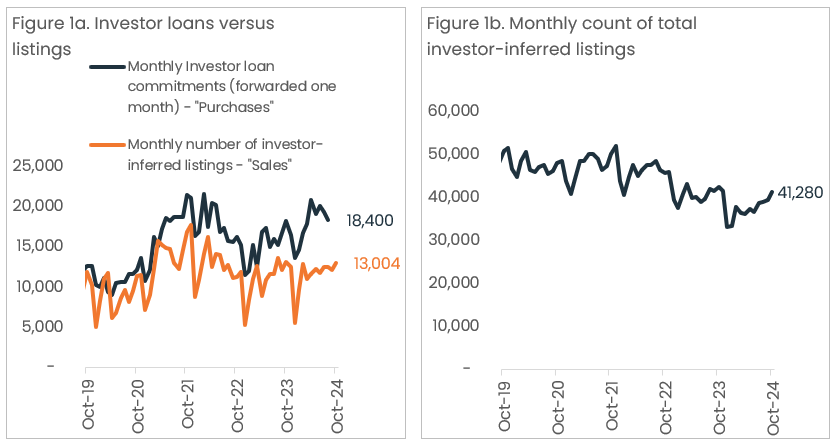

On the other hand, investment purchasers are on the rise. RBA data shows growth in investor housing credit has risen strongly, and ABS data shows the number of investor loan commitments in the year to September was around 212,500, up 18.8% on the previous 12-month period.

So which story is right? Or can both be true at the same time?

At a high level, investor demand looks stronger than investors “exiting” the market

One way of getting more insight on investment purchases and sales is by comparing the number of secured housing investment loans reported by the ABS, against the number of new listings that CoreLogic infers are investment properties coming up for sale.

The ABS data acts as a loose proxy for investment purchases, while CoreLogic data acts as a proxy for properties being relinquished by investors, by counting the number of properties listed for sale that have previously been advertised for rent. The metric doesn’t capture investors exiting the market by moving into their own investment property, nor will it count off market sales and rentals.

Investor inferred listings have been trending higher since March this year, to 13,000 but remain well below the peak of investor listings activity in November 2021. In November 2021, selling conditions were very strong, national home values had risen almost 25% in the space of a year, and even short-held investment properties were turning a strong profit.

Regional differences matter

The balance between new investment purchases, and current investment sales, is not as cut and dry by state, with elevated levels of new investment loans in high-growth markets, and more investor listings in low-growth markets.

In the year to September 2024, ABS loan commitments for investments grew 18.8% nationally, but most of that uplift was driven by NSW, QLD and WA. Figure 2 shows the highest growth in investment loans over the year has been concentrated in high capital growth areas, and that investment activity tracks strongly with value change. In both Victoria and Tasmania, where values have been in decline, the year-on-year uplift in investor loans was relatively small, at 5.1%.

The trend in new investment listings is also diverse. In October, new investor listings were around 3,800 in Victoria, accounting for 29% of the national figure, and up 10.6% on the previous five-year average. Meanwhile, investor listings were below the historic average in SA, QLD and WA where housing values have been rising rapidly. The investor loans and listings data is split out by state in Figure 3, showing the national trend of high investor purchases relative to sales is not evident everywhere.

In Victoria, the data supports the narrative that a relatively high level of investment dwellings are being listed for sale, while new investor loans secured is relatively subdued compared to previous years, and the national trend. Not only do investors in Victoria contend with high interest rates, but capital growth in the state is soft, and the reduced land tax threshold from the start of 2024 has increased holding costs for investors.

In Tasmania, there have been no significant changes to investment property taxes in 2024, but falling home values and rising interest rates may be prompting an exit from some investors. In October, new investment listings in Tasmania were 10.3% above the historic five-year average.

Interestingly, NSW investment listings were also 7.2% above average, but new investor demand is likely offsetting a loss in investment properties across the state.

It’s not just the location that is changing for investors

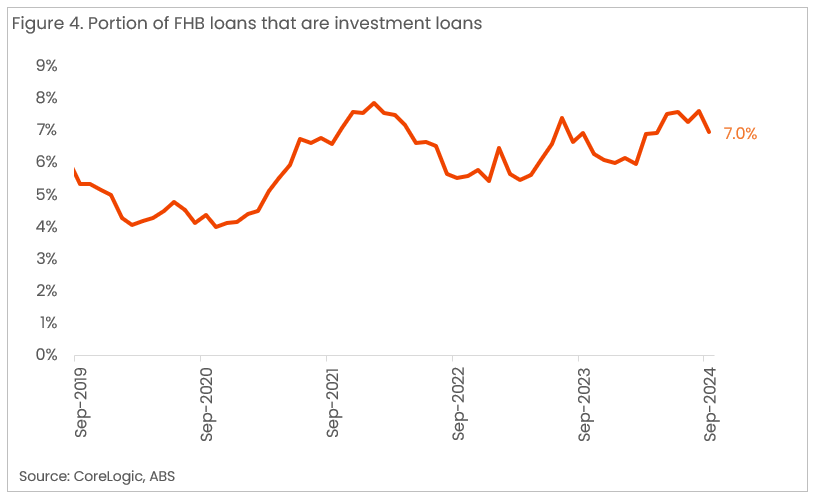

The stark changes in Australia’s economic environment over the past few years mean that the kinds of properties investors buy may be changing, and the kind of investors in the market may be changing too. The RBA noted a possibility that less leveraged investors may be taking the place of more highly-indebted ones. ABS loan data also suggests the portion of first home buyer loans for investment purchases has risen, though the underlying number remained very small in September 2024 (711 loans). This may be a function of some first home buyers viewing an investment property as a more affordable entry point to the housing market.

Despite the national trend showing strong growth in investment activity over the past year, there has been a slight easing in new loan commitments since April, and it is possible that new investor loan numbers soften further towards the end of 2024. This could be related to affordable investment opportunities with strong capital growth potential becoming scarcer following a period of high growth across lower price point properties. With interest rates potentially set to remain higher for longer than anticipated, interest rate reductions may already be priced into some high growth pockets. However, so long as the cash rate remains stable, this is more likely to result in a reduction in new investment purchases nationally, than an uplift in investor selling.

Meet Eliza Owen

Head of Residential Research Australia

Eliza Owen was appointed the Head of Research at CoreLogic Australia in 2020.

Full profile