Showing 1-15 out of 619 results

The biggest migration hot spots and the impact on housing trends

Head of Research Eliza Owen explores the highest migration regions in Australia and how it has impacted home values and rents.

Auction Market Preview - 28 April 2024

Auction volumes steady for fourth consecutive week

Population density: where is it the highest and what does it ...

In today's Pulse, CoreLogic research director Tim Lawless reveals the impact of population density on the housing market.

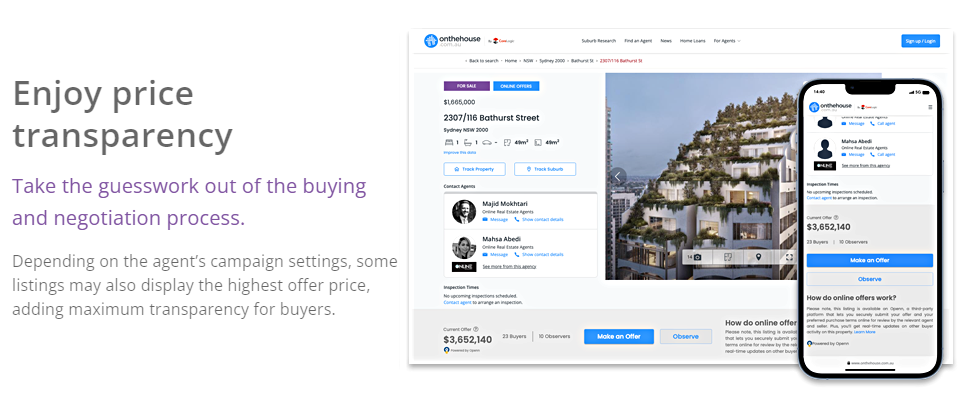

Can price transparency create better results?

To create greater transparency for buyers and sellers, Openn Offers is now available on OnTheHouse.com.au. Further digitising ...

Improvement in preliminary clearance rate across combined ...

The preliminary capital city clearance rate came in at 74.4% last week, up 1.7 percentage points relative to the previous week ...

Changing the perspective on first home buyer numbers

In today's Pulse, Eliza Owen examines the ABS's housing finance data, analysing the first home buyer segment's ...

Auction Market Preview - 21 April 2024

Capital city auction activity eases after a post-Easter bounceback

How do you get more appraisals from old data?

Regardless of your experience level as an agent, a common hurdle is figuring out what to do with legacy data. This includes ...

Preliminary clearance rate slips across similar auction ...

There were 1,952 auctions held last week, roughly on par with the week prior (1,985), but returning a lower preliminary clearance ...

4 x Townhouses Sold from a Digital Campaign

Gus asked Plezzel to create a digital advertising campaign that featured the key attributes of the development including the ...

Auction Market Preview - 14 April 2024

Auction volumes hold steady week-on-week across the combined capitals

3 Steps To Sell Digital Advertising To Your Vendor

When it comes to selling digital advertising to your vendor, it may feel like a challenge. Fortunately, there are just three key ...

Construction sector on road towards normalisation of costs

With detached dwelling approvals hitting a 12-year low in January, growth in national construction costs continued to stabilise in ...

Monthly Housing Chart Pack - April 2024

Here are the must know stats, facts and figures on Australia's residential property market for April 2024.

Solid bounce back in preliminary clearance rate

The preliminary combined capitals clearance rate recorded a solid bounce last week, rising to 75.9% from 71.1% the previous week ...